How Is the OpenSea SEA Token Launch Different From Past NFT Tokens?

OpenSea has been rumored to be “about to launch a token” since 2017. The most dramatic moment was 2022, when Blur entered the market and the community was convinced SEA was weeks away. The wait then lasted another four years. SEA finally went live in January 2026. This post walks through what happened, why the final structure landed where it did, and how the market received it. I break the event into three stages: before, during and after.

Two upfront notes. This is not investment advice. The airdrop claim window closed on February 7, so writing strategy now is pointless. What I want to preserve is a clean record of the launch as a paradigm sample, because the structure here will probably influence how large platforms launch tokens over the next one to two years.

Supply structure at a glance

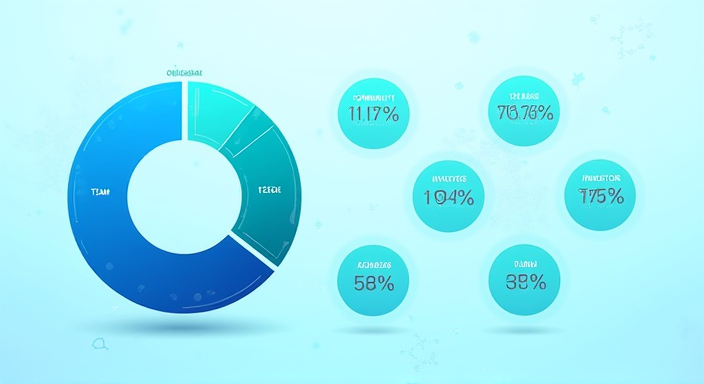

Per OpenSea’s published tokenomics:

- Total supply: 10,000,000,000 SEA (10 billion)

- Community: 50% (22% airdrop, 18% ecosystem fund, 10% market making and liquidity)

- Team: 18% (4 year linear vest, 12 month cliff)

- Investors: 17% (legacy 2024 Series C converted, 3 year linear, 6 month cliff)

- Foundation: 10% (SEA Foundation, Switzerland)

- Advisors and early contributors: 5%

A 50 percent community share is not extreme by 2026 standards. Friend.tech and Blur v2 both went above 60 percent. What sets OpenSea apart is that the 22 percent airdrop only goes to wallets with real trading footprint, with explicit exclusion of wash trading addresses.

The contested airdrop rules

The most debated part of the launch deserves its own breakdown:

- Eligibility floor: at least one real trade on OpenSea between January 2018 and December 2025.

- Volume weighting: ETH-denominated, capped at 50 ETH equivalent per wallet.

- Multi-chain coverage: Ethereum, Polygon, Arbitrum, Base and Solana all counted.

- Sybil filter: Trusta Labs’ on-chain sybil identification removed about 470,000 wallets.

- Creator multiplier: wallets that deployed original contracts received a 1.3x factor.

The biggest controversy was the 50 ETH cap. Whales argued this flattened their high-volume contribution to mid-tier user levels, effectively tilting airdrop value toward the long tail. CEO Devin Finzer’s response on X was direct: “We are rewarding breadth of participation, not a handful of whales.”

That same rule was later copied by Friend.tech v3 and several SocialFi projects, defining the 2026 “anti-sybil plus anti-whale” compression approach.

Market performance: 48 hours and 30 days

Splitting the post-launch tape into segments:

| Phase | Price range | Key events |

|---|---|---|

| Launch day | $0.42 – $0.71 | Binance, OKX, Coinbase listed simultaneously, FDV peaked at 7.1B |

| Days 2-7 | $0.38 – $0.55 | Early airdrop recipients gradually sold, daily volume tapered |

| Days 8-30 | $0.27 – $0.36 | Sideways consolidation, correlation with broader NFT market rose |

The first-day FDV of 7.1B landed at almost exactly half of OpenSea’s private-market valuation of 13B in early 2026, which tells you that the secondary market discount on NFT platform equity is still in effect. The trajectory is closely echoed by Blur’s own post-launch pattern.

What is the token actually used for

Reading the official tokenomics, SEA’s real utility comes down to three buckets:

- Fee discount: staking SEA tiers maker and taker fees down from 2.5 percent toward a floor of 0.5 percent.

- Creator incentives: creators can spend SEA to promote their work, similar to an on-chain paid placement model.

- Governance: Snapshot voting, currently open only to non-financial items such as fee structure and incentive allocation.

A crucial fact: SEA does not share trading fee revenue. Holding the token does not entitle you to a slice of platform income. This is the bright line the SEC drew during the 2024 and 2025 token litigation wave, and the OpenSea team chose the most conservative path.

What is most relevant to Web3 starter guide readers

A lot of readers care less about this specific project and more about how to participate in the “old platform launches a new token” pattern. Three practical observations:

- Real usage is the hard currency: every major 2026 airdrop treats wash trading as a penalty. Each genuine trade is worth more than volume farming.

- Cross-chain points get aggregated: OpenSea explicitly counted Solana and Polygon, signalling that your footprint across all chains on a platform should be treated as a single identity.

- Diminishing returns at the late edge: Blur’s launch airdrop was worth 2.3x what OpenSea delivered. The later you arrive in this category, the more airdrop value gets compressed.

Place this participation logic into the framing from the SocialFi starter and the picture sharpens. On-chain identity is becoming reusable across launches. Every real account is accumulating weight for the next drop.

The detail most worth remembering

If I could only keep one detail, it is that the SEA Foundation is incorporated in Zug, Switzerland. This means:

- OpenSea Inc (Delaware, USA) and the SEA token issuer (Swiss Foundation) are fully separated legal entities.

- The 18 percent team lockup is administered by the Swiss foundation.

- US users can interact with SEA’s protocol functions, but the US OpenSea entity does not actively distribute the token.

This is the de facto standard structure for a US-anchored crypto company launching a token in 2026. If Coinbase ever issues a token, it will almost certainly clone this template. In that sense, SEA’s significance extends beyond OpenSea. It is the compliance reference launch for large US platforms, and the issuances over the next year or two will use it as a baseline.

I will add a follow-up section on staking rate, governance participation and monthly active wallet turnover in next month’s 2026 major crypto events recap update.