How Does the Aave V4 Hub-and-Spoke Architecture Work?

On March 30, 2026, Aave V4 launched — exactly three years after V3. Between them: GHO, multichain expansion, a sustained encroachment by Morpho, and successive “next-gen lending” narratives. V4’s answer is hub-and-spoke: one unified liquidity hub and many independently configured spoke lending markets.

It can sound like jargon, but the logic is concrete — V4 solves two structural problems V3 accumulated during multichain expansion: liquidity fragmentation and rigid risk parameters.

Why V3 Had to Evolve

V3’s model is one pool holding all assets: USDC, ETH, wBTC, LSTs, GHO — all in one market with shared liquidation engine and reserves. Simple and liquidity-dense, historically Aave’s biggest advantage.

By late 2025, several tensions had become unresolvable:

- Risk profiles diverged dramatically. Mixing ETH with long-tail L2-native tokens forced parameters to the most conservative setting, throttling blue-chip capital efficiency.

- Multichain deployment amplified fragmentation. Separate markets across Ethereum, Arbitrum, Optimism, Base, Polygon — siloed liquidity, idle assets that could not be cross-deployed.

- Morpho’s “isolated markets + curator vaults” ate the curated-strategy layer. See How to Use Morpho Curated Vaults.

- GHO needed a deeper foundation. “Yet another asset in the pool” cannot scale a stablecoin.

V4 hub-and-spoke is the integrated answer.

What the Hub Does

Three responsibilities:

- Asset custody and liquidity pooling. All spoke deposits live in the hub contract; spokes hold claims against the hub. Spoke A deposits can be reused by spoke B.

- Unified oracle layer. Hub maintains the oracle registry; all spokes share the same feeds.

- GHO minting and liquidation. GHO is no longer an asset in a market — it is a hub-level debt claim. Any spoke can let users borrow GHO depending on its collateral config, while GHO supply, rates and stability fees are managed at the hub.

The result resembles “a clearing layer behind several retail storefronts”. Curve’s multi-pool design and Uniswap V4’s hook model head in the same direction — separate invariant core from variable strategy.

What a Spoke Is

Each spoke has its own: supported asset list, LTV / liquidation thresholds / incentives, rate curve, isolation config, governance controller (Aave DAO or authorized third-party curator).

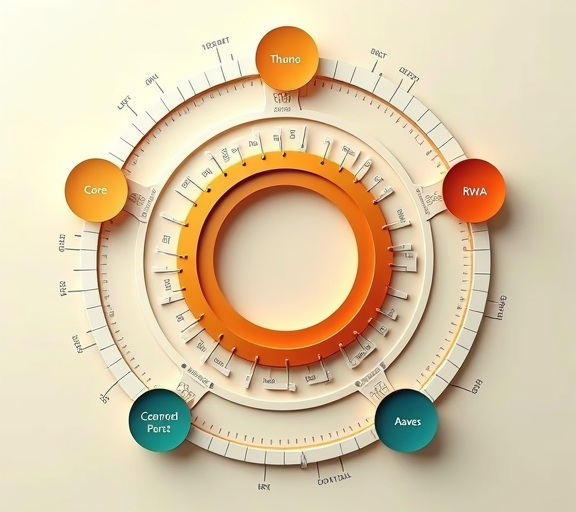

Sample spokes live since V4 launch:

| Spoke | Target | Collateral | Borrowable |

|---|---|---|---|

| Core | Mainstream | ETH, wstETH, wBTC, USDC, USDT | All major + GHO |

| LRT | LRT holders | weETH, ezETH, rsETH | ETH, USDC, GHO |

| RWA | Institutional | Tokenized treasuries (Ondo, Maple) | USDC, GHO |

| Stablecoin | Arbitrageurs | USDC, USDT, DAI, USDe, sUSDe | Any stable + GHO |

| Long-tail | High-risk users | Long-tail tokens | ETH, USDC |

Crucially, each spoke’s risk parameters can be aggressive or conservative without affecting other spokes. Long-tail bad debt is contained inside Long-tail Spoke and does not bleed into Core.

This borrows Morpho’s isolated-market idea, but V4 layers it on top of hub-level liquidity pooling, sidestepping Morpho’s main weakness of severely fragmented liquidity per market — new spokes can borrow from idle hub liquidity on day one.

Depositor and Borrower Experience

Depositors: UX similar to V3, but two underlying changes — your deposit can be lent into other spokes via the hub, so yield reflects hub-level redistribution across all spokes (smoother); and risk is isolated per spoke (Long-tail bad debt does not hit Core).

Borrowers: Different spokes offer different terms. Holding LRTs? LRT Spoke offers 5–10 percentage points higher LTV than a V3-style mixed market. GHO stability fees are dynamically adjusted by the hub, not by DAO vote each time. Cross-chain borrowing becomes a protocol primitive (collateralize on chain A, borrow on chain B), see Top DeFi Protocols Overview 2026.

Comparison

| Protocol | Architecture | Pooling | Isolation | Best fit |

|---|---|---|---|---|

| Aave V3 | Single big pool | Yes | Weak | Blue chips |

| Aave V4 | Hub + spokes | Hub + spoke isolation | Strong | Full spectrum |

| Morpho | Isolated markets + curator vaults | No | Very strong | Curator-led |

| Spark | V3 fork + Sky gov | Yes | Weak | DAI/USDS centric |

| Compound V3 | Single borrow asset per market | Partial | Medium | Simple lending |

V4 positions itself as a hybrid between Morpho’s isolated-market flexibility and V3’s liquidity depth. Success depends on governance throughput and whether the hub becomes a new bottleneck. New to Aave? Start with What Is Aave Lending.

Risks and Open Questions

- Hub is a new single point of risk. A hub contract bug or oracle exploit hits all spokes simultaneously.

- Cross-spoke rate curves are still maturing. Hub liquidity rebalancing under stress is untested.

- GHO carries more weight. A depeg would propagate beyond stablecoin markets. Sword cuts both ways.

- Governance load goes up materially. If DAO throughput cannot keep pace, V4’s flexibility advantage erodes.

V4 has run two months without major incident, but those two months were calm. A lending protocol’s real test comes in extreme markets — V4’s next milestone is surviving a meaningful liquidation cascade.

Practical Spoke Selection

- Blue-chip collateral, liquidity matters: Core Spoke, default.

- LRT holdings, leveraging ETH yield: LRT Spoke, watch LRT depeg with spoke liquidation incentive.

- Stablecoin arbitrage: Stablecoin Spoke.

- Long-term holder generating cash flow: any spoke deposit + small GHO borrow.

- Institutional / compliance-heavy: RWA Spoke, KYC required.

Common mistake: do not enter a spoke just because LTV is high. High LTV often pairs with aggressive liquidation thresholds. Read the spoke’s risk parameter doc first.

Implications for the Lending Sector

- Aave reclaims differentiation against Morpho. V4 brings curated-strategy capability back inside Aave. Morpho still wins on permissionless market creation, since V4 spokes require governance approval. Real competition, two philosophies.

- GHO graduates from “another stablecoin” to “protocol-level debt instrument,” moving toward DAI/USDS positioning.

- Cross-chain consolidation pressure intensifies. V4 makes within-protocol multichain liquidity feasible, forcing competitors to replicate or commit to Morpho-style isolation.

- Curated-vault product space contracts. Yearn V3, Mellow LRT vaults — pushed toward narrower, more active niches. See DeFi Yield Strategies 2026 - Structured Products.

V4 is not the endpoint. Watch the hub’s cross-chain messaging choices (LayerZero, CCIP, Hyperlane, primary and fallback) and how the hub-level liquidation and rebalancing mechanism holds up in the first genuine liquidity crunch. Hub-and-spoke is Aave’s biggest 2026 bet — either it defines the next lending standard, or it becomes another DeFi case study of “correct design, outpaced execution.” Both outcomes have nonzero probability.