Ethereum Liquid Staking Derivatives in 2026: Real Numbers, Real Yields, and the New Risks Most Users Miss

I bought my first stETH in 2021. Back then Lido held about 90% of the liquid-staking market and stETH was effectively an “index ETF for staked ETH.” Five years on, the picture is unrecognisable. stETH still exists but holds under 50% share. Rocket Pool went institutional. Frax brought its algorithmic stablecoin playbook to LSDs. Restaking layered on top of everything and made the whole sector simultaneously more interesting and more dangerous.

This piece does three things. It updates the data for May 2026, breaks down where yield actually comes from, and identifies the three risk categories we mostly did not worry about in 2023.

Liquid staking, plainly explained

If you are new, start with what is liquid staking lsd. The short version:

- You delegate ETH to a protocol like Lido, Rocket Pool, or Frax.

- The protocol stakes it through validators and earns rewards.

- You receive a derivative token (stETH / rETH / frxETH) representing your claim on the underlying ETH plus rewards.

- The derivative trades on DEXes, can be used as collateral in lending markets, and earns LP fees. That is the “liquid” part.

The point is capital efficiency. The 32 ETH that used to be locked can now both earn staking rewards and continue working in DeFi.

For a deeper comparison between Lido and Rocket Pool see lido vs rocket pool.

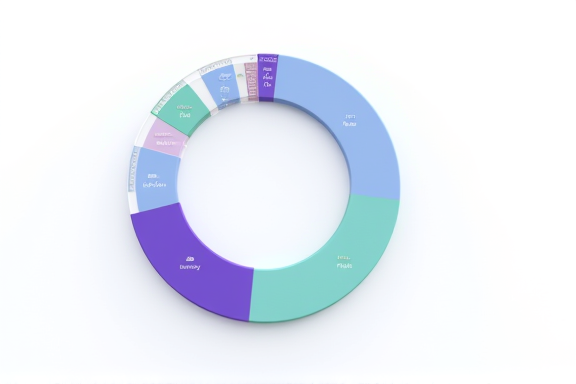

May 2026 market share snapshot

Numbers below pulled from Dune, DefiLlama, and project dashboards around May 20, 2026:

| Protocol | Derivative | Approx ETH staked | Share | Operator model |

|---|---|---|---|---|

| Lido | stETH / wstETH | ~9.6M | ~48% | Permissioned curated operators |

| Rocket Pool | rETH | ~2.4M | ~12% | Fully permissionless (8 ETH minimum) |

| Frax | frxETH / sfrxETH | ~1.1M | ~5.5% | Whitelisted by Frax DAO |

| Coinbase | cbETH | ~0.9M | ~4.5% | Single custodian |

| Binance | wBETH | ~0.8M | ~4% | Single custodian |

| Other LSDs (LRTs excluded) | — | ~5.2M | ~26% | Varied |

Key shift: Lido’s share of all ETH staking fell from a peak ~32% in 2023 to ~28%; its share among LSDs fell from ~75% to ~48%. Three drivers:

- Community pressure against Lido dominance. Large DeFi treasuries are actively diversifying.

- Rocket Pool’s Saturn upgrade in Q4 2025 dropped the minimum node bond to 8 ETH, attracting retail operators.

- Restaking platforms (Ether.fi and similar) diverted flow that would otherwise have gone to Lido.

Where the yield really comes from

Most beginners assume LSD APR equals “ETH staking APR.” It is actually three stacked components:

- Base staking yield. Validator consensus rewards plus MEV. Around 2.8% APR on mainnet in May 2026.

- Protocol fee (negative). Lido takes 10%, Rocket Pool around 14%, Frax variable.

- Secondary yield on the derivative (positive). You can collateralize stETH on Aave to lever up, or hold sfrxETH for additional fee splits.

Net result: a regular user holding stETH without leverage sees roughly 2.5-2.6% APR, very close to direct staking. With Pendle PT/YT splits or stETH/ETH LP, the theoretical range stretches to 4-7% but with extra risk.

For how Pendle splits LSDs into PT and YT see the yield tokenization section of defi yield strategies 2026 structured.

Three risk categories you must take seriously in 2026

We did not worry seriously about any of these in 2023. Each has now produced at least one near-miss.

Risk 1: depeg events are no longer purely liquidity events

The famous June 2022 stETH dip to 0.93 ETH is history. A sharper, shorter event hit in December 2025, when a major lending protocol exposed an oracle-lag bug and triggered a cascade, briefly knocking stETH to 0.96 ETH before recovery.

New-generation drivers:

- Lending plus LSD leverage loops. Many users collateralize stETH, borrow ETH, restake, recollateralize, looping 5-7x. A one-second oracle lag can cascade.

- Restaking exposure. Your stETH validator may also be running AVS duties, adding chronic slashing risk.

- Wrapped versions on L2. wstETH on Arbitrum or Base has thinner liquidity than mainnet, making depegs easier locally.

Background reading: lido stETH depeg history and mechanism.

Risk 2: restaking layers compound the risk

Restaking lets the same ETH provide security to additional AVSes on top of base staking, in exchange for more yield. It sounds great. In practice it stacks risk:

- Chronic slashing. If an AVS validator gets slashed 1% due to a software bug, your LSD takes a 1% hit.

- Weak AVS economics. Some AVSes do not yet have a security budget large enough to cover catastrophic failure.

- Liquidity nesting. LRTs like weETH are derivatives of derivatives, making the leverage chain longer.

See restaking real risks cases 2026 for actual incident write-ups.

Risk 3: regulators are sharpening their view

Both the SEC and ESMA made formal statements about LSDs during 2025:

- United States. Clarity Act granted partial exemptions, but Lido and Rocket Pool style protocols land in a “potential staking security” gray zone with disclosure obligations ahead.

- European Union. MiCA phase two pulls LSD derivative tokens under the crypto-asset-service umbrella, requiring whitepapers from issuers.

- Hong Kong and Singapore. Friendlier so far, but require KYC at the custodial node layer.

For the regulatory background, see us sec crypto regulation stance and what is mica eu regulation.

What to do depending on your profile

- Long-term holder. Direct stake or buy stETH and hold. Do not run leverage loops.

- DeFi player. sfrxETH or wstETH LP is fine, but keep leverage under 2x and stay in mainnet or Arbitrum blue-chip markets.

- Higher risk tolerance. Try LRTs, but cap any single LRT at 20% of total ETH exposure, and review the underlying AVS set monthly.

The 2026 watershed for LSDs

In 2021, LSD meant “lazy staking.” In 2026 it is a full financialization stack: LSD, LRT, PT/YT, structured yield, institutional tranches.

Headline yields look higher, but the risk became deeper and harder to intuit. What you hold may no longer be a clean shadow of ETH. It may be a composite product with four or five layers of financial structure. Each layer is reasonable on its own. The stack is not always reasonable.

If you just want plain ETH yield, stake directly or hold stETH untouched. Skip the PT/YT and leverage loops. If you want more, the important question is not “what APR” but “where in the stack am I earning, and which layer breaks first if something goes wrong.”